Updated June 2026

What Is Uninsured Motorist Coverage Insurance?

Uninsured Motorist Coverage steps in when another driver causes an accident and either has no insurance or lacks enough coverage to pay for your injuries and damage. It covers your medical expenses, lost wages, pain and suffering, and in some cases vehicle repair costs when the at-fault driver cannot pay. South Carolina law requires insurers to offer this coverage at the same limits as your liability policy, and you must sign a rejection form if you want to decline it. For suspended drivers working toward reinstatement, maintaining UM coverage during suspension can prevent gaps that trigger higher premiums once you're back on the road.

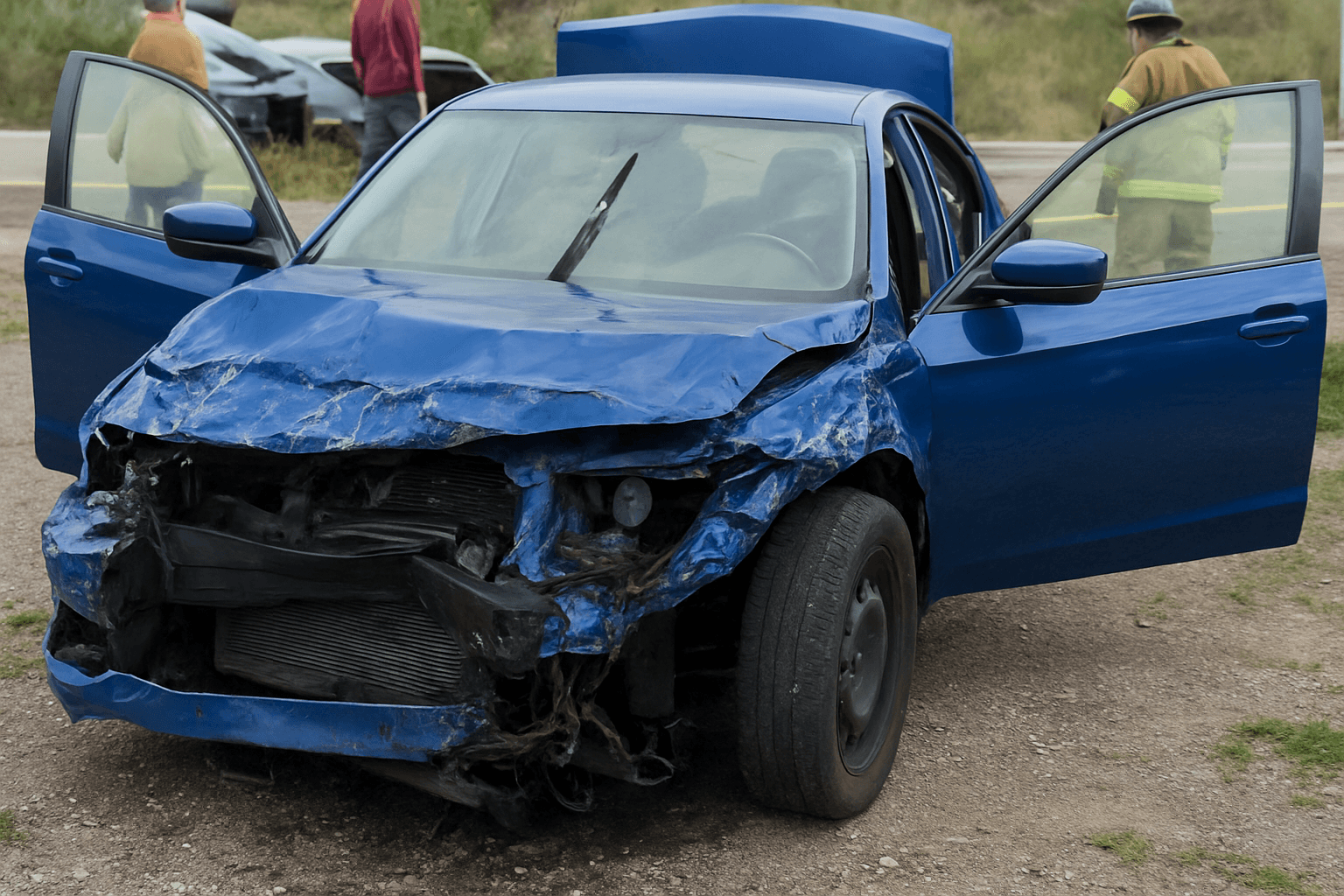

- A driver sideswipes your car on I-26 near Columbia and flees without stopping. You have $8,500 in medical bills from the emergency room and follow-up care, plus $4,200 in vehicle damage. Your Uninsured Motorist Bodily Injury coverage pays the $8,500 medical expenses up to your policy limit. If you carry optional Uninsured Motorist Property Damage coverage with a $3,500 limit, it pays that amount toward repairs, and you cover the remaining $700 out of pocket or through collision coverage if you have it.

- An uninsured driver rear-ends you at a red light in Charleston, causing $12,000 in medical bills and $6,800 in vehicle damage. You carry the state minimum UM coverage of $25,000 per person for bodily injury. Your UM coverage pays the full $12,000 in medical costs. Without UM Property Damage or collision coverage, you pay the $6,800 vehicle repair yourself or absorb the loss if the car is totaled and the uninsured driver has no assets to pursue in court.

- A driver with only $25,000 in liability coverage runs a stop sign and T-bones your car in Greenville, causing $42,000 in medical expenses. The at-fault driver's insurance pays their $25,000 limit. If you carry $50,000 in Underinsured Motorist coverage, your policy pays the remaining $17,000. If you carry only the minimum $25,000 UM, your coverage pays nothing because the at-fault driver's policy already met that threshold, leaving you $17,000 short.

Who Needs Uninsured Motorist Coverage Insurance?

Suspended drivers working toward reinstatement should carry Uninsured Motorist Coverage because South Carolina's 13% uninsured driver rate means roughly one in eight accidents involves a driver who cannot pay. If you're required to carry SR-22 insurance, your insurer will file the SR-22 on a policy that already includes UM unless you sign a rejection, and dropping it later can create a coverage gap that delays reinstatement. Drivers without collision coverage—common among those on non-owner SR-22 policies—benefit from adding UMPD because it's often the only way to recover vehicle repair costs when an uninsured driver hits you.

Calculate your health insurance deductible and out-of-pocket maximum, then compare that to the annual cost of UM coverage. If an uninsured driver hits you and causes $15,000 in medical bills, would your health plan leave you with less than $200 in costs? If yes, and you don't own a car, reject UM. If your health plan has a $5,000 deductible or high coinsurance, UM coverage costing $12/month pays for itself in a single accident.

How Much Does Uninsured Motorist Coverage Insurance Cost?

Uninsured Motorist Coverage typically adds $8–$18 per month to your premium in South Carolina, or approximately $96–$216 annually, depending on your chosen limits and driving history.

- Your UM coverage limits—choosing $50,000/$100,000 instead of the state minimum $25,000/$50,000 increases cost but closes the gap when at-fault drivers carry minimal insurance.

- Your zip code and county—areas with higher rates of uninsured drivers, such as parts of rural South Carolina where approximately 13% of drivers lack insurance, typically see higher UM premiums.

- Your driving record and suspension history—carriers price UM coverage higher for drivers reinstating after DUI or points-related suspensions because those drivers statistically file more claims.

- Whether you add Uninsured Motorist Property Damage coverage—adding UMPD with a $25,000 limit typically costs an additional $4–$9 per month.

- Your deductible choice for UMPD—South Carolina allows deductibles of $200, $250, or $500 on property damage claims, with lower deductibles increasing your monthly cost.