Updated June 2026

What Is Liability Insurance Insurance?

Liability insurance is the foundation of auto insurance—it covers the other driver's medical bills, vehicle damage, and legal costs when you cause an accident. South Carolina law requires bodily injury liability of $25,000 per person and $50,000 per accident, plus $25,000 in property damage liability. If you're reinstating after a suspension for lapsed insurance, DUI, or excessive points, proof of liability coverage is mandatory before the DMV will process your reinstatement. Non-owner liability policies exist specifically for drivers who need coverage to satisfy reinstatement requirements but don't own a vehicle.

- You rear-end a stopped car at a traffic light in Columbia. The other driver has $18,000 in medical bills and $9,000 in vehicle damage. Your 25/50/25 liability policy pays the full $27,000 because it falls within your per-person bodily injury limit ($25,000) and property damage limit ($25,000). Your own vehicle damage—$4,500 to your front bumper and radiator—is not covered. You pay that repair bill yourself or file a collision claim if you carry that optional coverage.

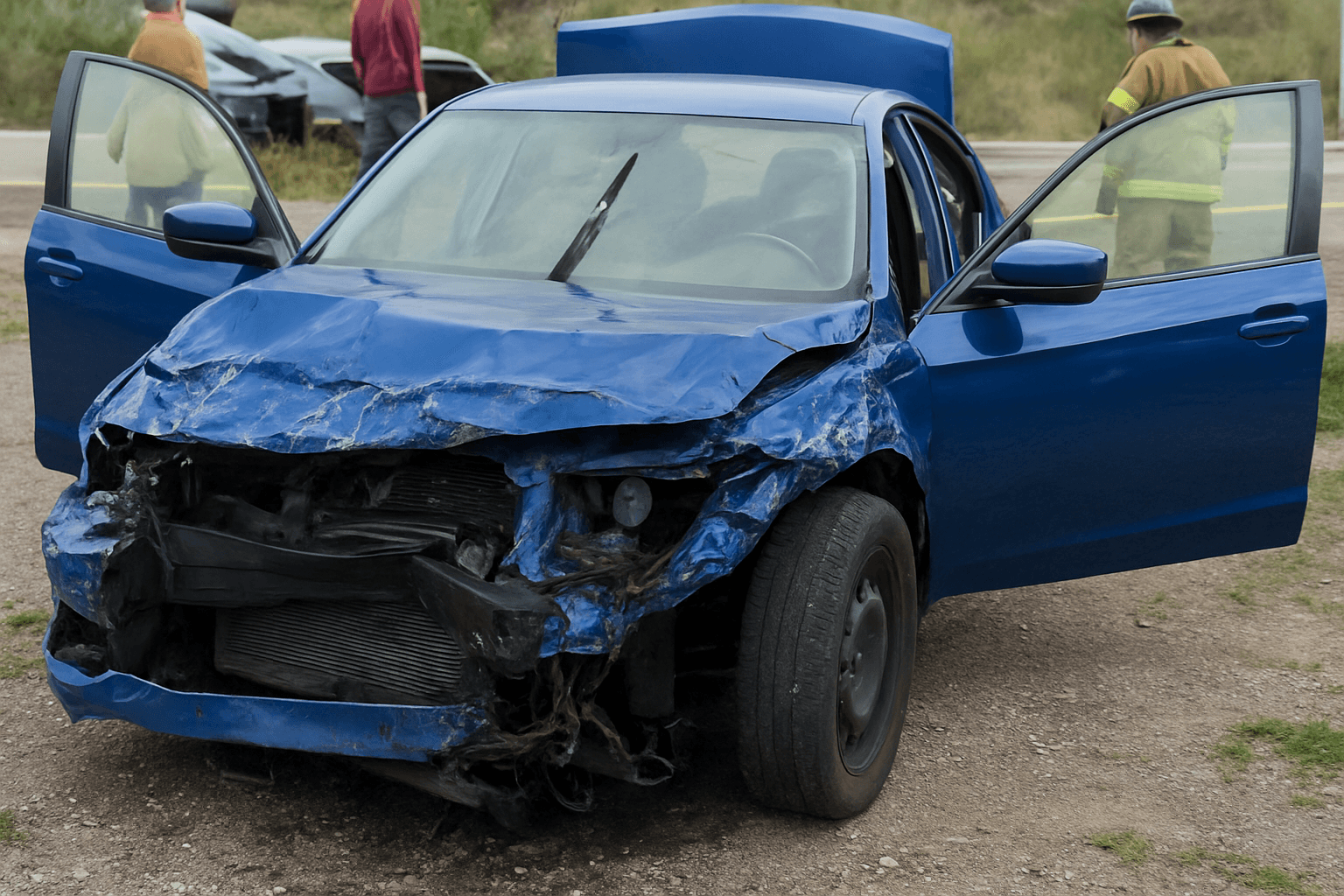

- You cause a three-car pileup on I-26. Two injured drivers each have $40,000 in medical bills. Your bodily injury limit is $25,000 per person, so your insurer pays $25,000 to each driver—$50,000 total, which maxes out your per-accident limit. You are personally liable for the remaining $30,000 ($15,000 per injured party). The other drivers can sue you for the unpaid amount, and a judgment can lead to wage garnishment or asset seizure.

- Your license is suspended for six months due to a DUI. You sold your car and don't plan to drive during suspension, but South Carolina requires continuous liability coverage to avoid extending your suspension period. You purchase a non-owner liability policy for $35/month. It satisfies the state's coverage mandate and allows your insurer to file the required SR-22 form. When your suspension ends, you present proof of continuous coverage and the DMV processes your reinstatement without additional penalties.

Who Needs Liability Insurance Insurance?

You need liability insurance if you are reinstating your license after any suspension related to insurance lapse, DUI, points accumulation, or unpaid fines in South Carolina. It is also required if you plan to drive any vehicle, even one you don't own—borrowed cars, rental cars, and employer vehicles all require you to carry liability when your license is valid. Non-owner liability is the correct product if you don't own a car but need coverage to satisfy reinstatement or SR-22 filing requirements.

If your suspension letter or reinstatement notice lists proof of insurance or SR-22 filing as a requirement, you must carry liability coverage for the full reinstatement period—even if you're not driving. If you don't own a vehicle, request a non-owner liability quote. If you do own a vehicle but won't drive during suspension, confirm whether South Carolina allows you to pause coverage without extending your suspension—most suspension types do not allow this, and a lapse restarts your compliance clock.

How Much Does Liability Insurance Insurance Cost?

South Carolina minimum liability (25/50/25) typically costs $45–$85/month for standard-risk drivers, or $540–$1,020/year. Drivers reinstating after suspension often pay $90–$180/month due to lapse history or violations.

- Suspension cause—DUI violations increase liability premiums 80–150% compared to lapse-only suspensions.

- SR-22 filing requirement—adding the SR-22 form to your policy costs $15–$50 filing fee, but the suspension history drives the larger rate increase.

- Coverage history—a lapse longer than 30 days typically adds 20–40% to your base liability rate.

- Liability limits chosen—increasing to 50/100/50 coverage costs an additional $15–$35/month but protects you from personal liability in serious accidents.

- Zip code—Charleston and Columbia metro areas have higher liability rates due to accident frequency and congestion.

- Non-owner vs standard policy—non-owner liability costs 30–50% less than standard auto liability because there's no vehicle to insure for collision or comprehensive risk.